Lessons from Connecticut’s Income Tax: A Cautionary Tale

In 1991, Connecticut implemented a flat income tax of 4.5 percent. The income tax promised to stabilize tax revenues by replacing the volatile state capital gains tax and was to accompany a meaningful spending cap. Over the past 26 years, the income tax rate has been raised and brackets have been added multiple times. Connecticut has harvested $126 billion from the income tax since 1991. While a boom for state coffers, the income tax has created several negative long-term economic consequences.

Connecticut’s income tax now creates some of the very policy problems it was intended to fix with a high top marginal rate, a large degree of progressivity in its structure and growing reliance on income tax revenue. Cyclical fluctuations in the market heavily influence income tax revenues by allowing legislators to expand spending during bull years. This higher level of spending has added to the arguments of those who wished to raise taxes in the bear years. They have been largely successful in securing increases. Since implementation, the top marginal rate has been increased four times up to 6.99 percent in 2017.

Income taxes suffer from a fundamental flaw – they are more heavily impacted by market cycles than broad-based consumption and property taxes. The top marginal rate and level of progressivity have quickly grown, the structural stability of the income tax has weakened. As a result, the income tax has become the primary source of state revenue.

The capital gains tax accounted for 9.21 percent of total tax revenue, on average between 1980 and 1991. The personal income tax, which replaced the capital gains tax, comprised nearly 53 percent of total tax revenue by 2016. In effect, any stability gained from eliminating the volatile capital gains tax was largely negated by displacing the role of the sales tax. Before and after the implementation of the income tax, the sales tax has been the most stable source of tax revenue. The percentage decline in sales tax revenue was just half that of the percentage decline in income tax revenue during the recessions of 2002 and 2008.

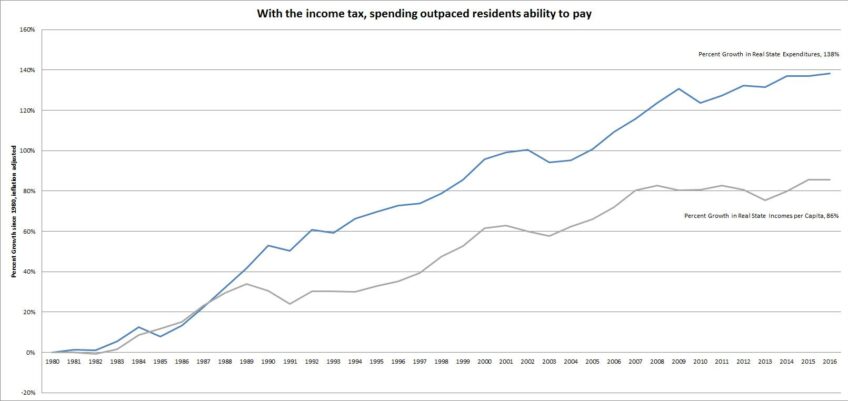

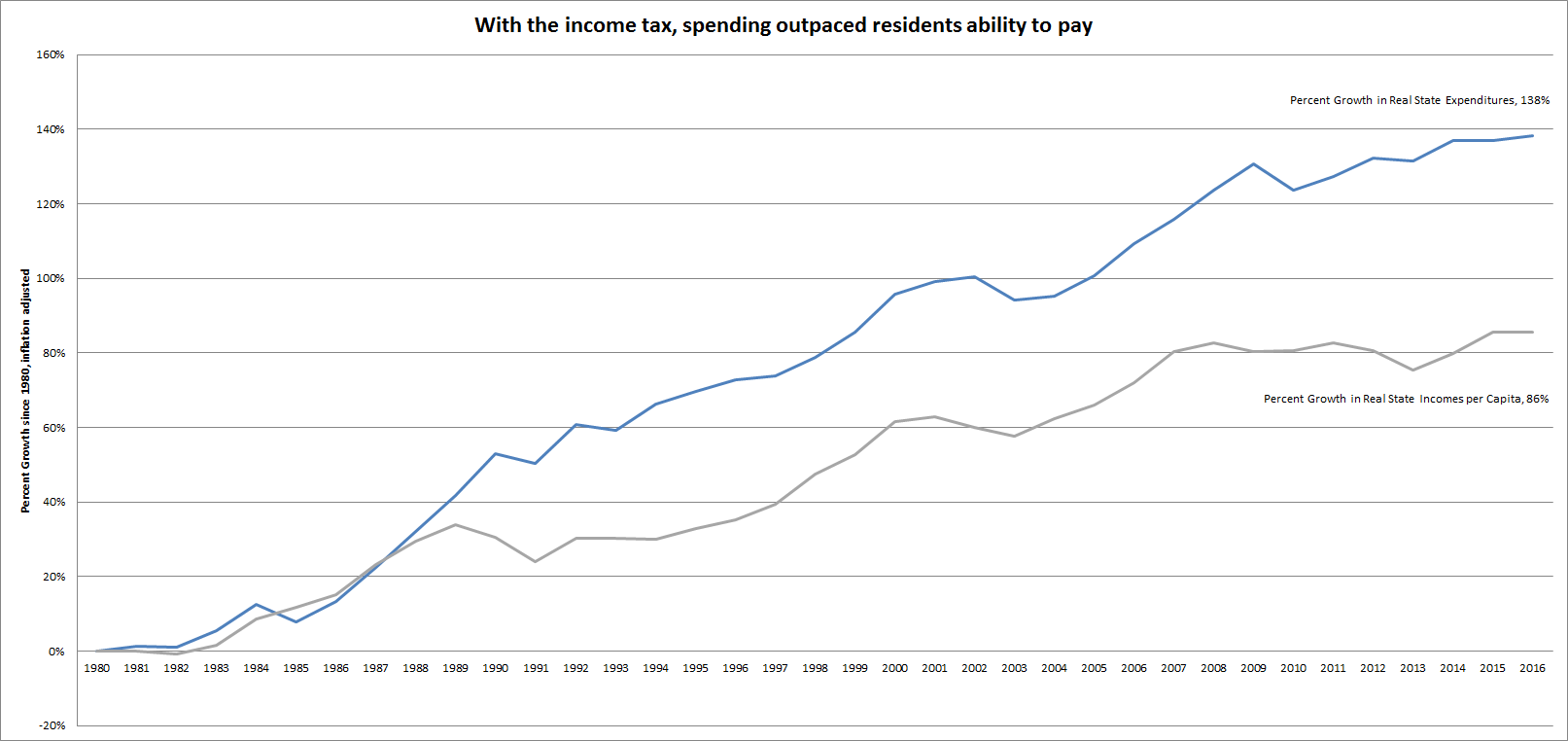

Revenue volatility from the newly introduced income tax played a central role in spurring on reckless state spending. Between 1980 and 1990, state expenditures per capita grew at roughly the same rate as state income per capita. After 1991, state expenditures began to grow much faster than the incomes generating tax revenue that supports expenditures. State expenditures rose 138 percent whereas incomes grew a mere 86 percent between 1980 and 2016. Ironically, politicians use rapid increases and decreases in income tax revenue as alternating excuses to justify increases in state expenditures.

During boom years, an influx of tax revenue enables legislators to expand spending. But during economic downturns, the diminished revenue stream is used by these same legislators as a justification for tax increases. State government spending grew two times faster than inflation plus population between 1991 and 2014.

Income tax revenue often expands at a greater rate than economic growth, leading politicians to ramp up spending during economic booms. This same revenue stream can stagnate and contract more sharply than broader output measures during economic doldrums. During these difficult economic times, revenue generated from existing income tax fails to fund the elevated level of government spending. Politicians then call for tax increases to avoid the threatened harm from spending reductions. The corresponding tax increases result in personal incomes declining far more than any reductions in state expenditures. After three recessions in the years following implementation of the personal income tax, the state now consumes 28 percent more of residents’ income compared to 1980.

For years now, residents and business have been leaving the state in response to deep budget deficits and a heavy tax burden. Connecticut had the largest tax hike in the state’s history in 2011. Because of this hike taxes increased the top marginal rate and steepened income tax progressivity. Between 2011 and 2013, domestic outmigration cost the state an average of $60 dollars of adjusted gross income per second. An even more dramatic outflow occurred after the 2015 tax increase—the second largest tax increase in state history. Despite the hike in effective income tax rates, 2016 income tax revenue came in $653 million dollars lower than projected and an astounding $279 million dollars below the prior year’s collections. Residents certainly vote with their feet in response to increases in marginal tax rates, particularly when they have no-income-tax alternatives like Florida.

Progressivity in the code certainly exacerbates the damage from an income tax. Instability of revenue becomes more pronounced by relying on fewer taxpayers for a greater portion of tax revenue. New Jersey’s income tax offered a dramatic case of this when a single taxpayer moved and reduced projected revenue by tens of millions of dollars. Connecticut is similarly becoming increasingly reliant on a dwindling pool of high-income earners. Residents with high incomes and or large assets are more mobile and therefore able to avoid income tax increases by moving to Florida, North Carolina or even Massachusetts.

After being severely stung by the recent departures of General Electric and Aetna, many leaders in Connecticut have realized the status quo is not sustainable. Currently, the state ranks 46th in the economic outlook ranking in Rich States, Poor States. 43rd in the State Business Tax Climate Index. 44nd in the Small Business Tax Index and 43rd in the Annual State Competitiveness Report. It is clear that Connecticut’s adoption of an income tax has produced strikingly bad results for the hardworking taxpayers of the Constitution State.

The income tax is the primary cause of the ongoing budget crises rather than a solution. Long-term growth requires a pro-growth strategy. On the spending side, the State Budget Reform Toolkit outlines a 13-step recovery program. The first step is for elected officials to recognize the problematic nature of the current budget system. On the revenue side, a shift away from harmful taxes on income and capital is needed. Replacing these with broader, flatter and lower property and consumption taxes will spur growth and foster stability. Connecticut still holds the potential to be an exceptional place to live, raise a family and retire. But the income tax impedes the prosperity necessary to actualizing this promise.