ALEC Releases New Report Examining the Effect of State Taxes on Charitable Giving

Charity is a crucial component of efforts to address societal challenges and help individuals thrive. From religious organizations to community charities, philanthropic donations drive the institutions of civil society and enable communities to develop around a greater sense of shared purpose. Despite this important role, charitable giving is rarely addressed in discussions around public policy—especially state tax policy.

The new State Factor: The Effect of State Taxes on Charitable Giving analyzes the interaction between state taxes and charitable giving through data from the Internal Revenue Service (IRS) and advanced economic analysis. While many factors certainly influence an individual’s choices about donating to charity, there are broad policy choices that can encourage higher rates of growth in charitable giving.

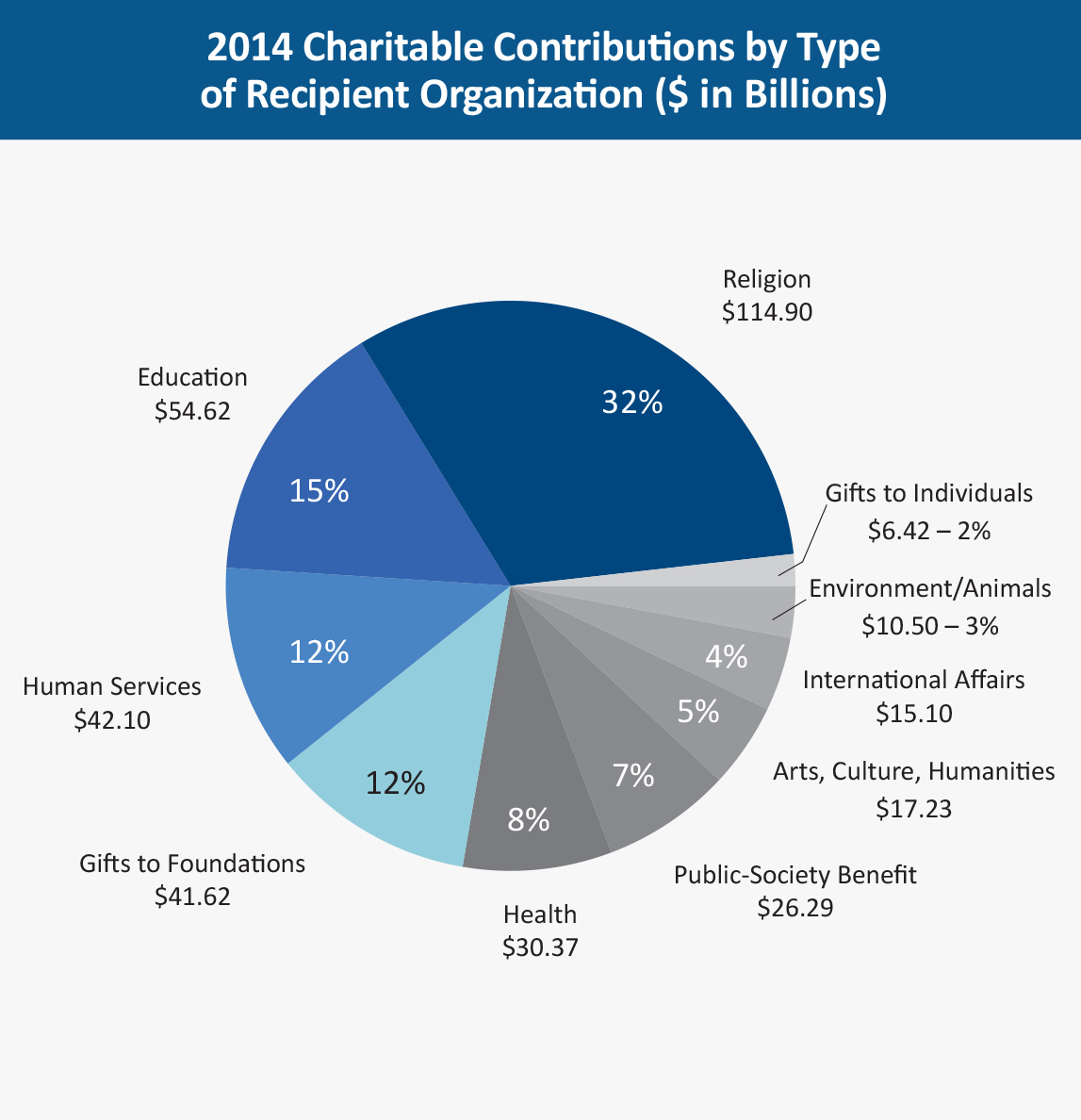

The study first outlines the broad picture of philanthropy across the nation. According to the National Center for Charitable Statistics, there are currently 1,507,231 tax-exempt organizations operating in the United States. In 2014, total charitable giving was $358.38 billion according to estimates by Giving USA, or about 2.1 percent of total GDP. The National Center for Charitable Statistics estimates that in 2012, 64.5 million people, about 26.5 percent of the U.S. population, volunteered at least once. Overall in 2012, the Center estimates 12.7 billion hours were spent volunteering, with an estimated valuation of $259.6 billion. The social impact of these efforts is substantial.

Additionally, we note the states that are giving the most in charity per dollar of state income and the states that are having the fastest growth in charitable giving. We look at this data both between 1997 and 2012, which is the full dataset available from the IRS, as well as 2008 to 2012 for a shorter-term perspective on the state of charitable giving related to the great recession. Those full, long-term results are displayed below.

- Most Generous States per Dollar of Income in Descending Order, 1997-2012: Utah, Wyoming, Georgia, Alabama, Oklahoma, South Carolina, Maryland, Idaho, North Carolina, Mississippi.

- Least Generous States per Dollar of Income in Descending Order, 1997-2012: Ohio, Wisconsin, New Mexico, Rhode Island, Vermont, Alaska, Maine, New Hampshire, North Dakota, West Virginia.

- Fastest Growth in Total Charitable Giving in Descending Order, 1997-2012: Wyoming, Texas, South Dakota, Montana, North Dakota, Nevada, Oklahoma, Georgia, Kansas, Washington.

- Slowest Growth in Total Charitable Giving in Descending Order, 1997-2012: Pennsylvania, Indiana, Wisconsin, New Hampshire, Rhode Island, New Jersey, Delaware, Ohio, Maine, Michigan.

Most notably, the study uses the tools of econometric statistical analysis to attempt to rigorously determine the strength and nature of the relationship between state taxes and charitable giving. The data show that the link is statistically strong in correlation and notable in size. Those results are summarized below. Note that total state charitable giving as a percent of income ranges from roughly 5.2 percent down to 1.15 percent across states and years.

- State Personal Income Tax Burden

- Growth: Considering the growth rate of charitable giving and growth rate of the state personal income tax burden, a 1 percent increase in a state’s personal income tax burden is associated with a 0.35 percent decrease in the state’s rate of charitable giving as a percent of total state income.

- Level: Considering the level of charitable giving and the level of the state personal income tax burden, this research found that an increase in personal income tax burden of roughly 1 percentage point of total state income results in a roughly 0.10 percentage point decrease in measured charitable donations as a percent of income.

- Total State Tax Burden

- Growth: Considering the growth rate of charitable giving and growth rate the total state tax burden, a 1 percent increase in a state’s total tax burden is associated with a 1.16 percent decrease in the state’s rate of charitable giving.

- Level: Considering the level of charitable giving and the level of the total state tax burden, this research found that an increase in total tax burden of roughly 1 percentage point of total state income results in a roughly 0.09 percentage point decrease in measured charitable donations.

As it becomes clear that a state’s tax and fiscal policy climate has a significant effect on rates of charitable donations, with higher taxes generally correlating with less philanthropy, it is important that discussions about tax policy also take into account these effects. Charity is uniquely equipped to engage a wide variety of social concerns and challenges. In better understanding these effects and tradeoffs, state policymakers can more effectively make decisions to respect the hardworking taxpayers of their state.